Question: What are some pros and cons of buy now, pay later loans?

NCSS: Production, Distribution, and Consumption

Common Core: R.8

Shutterstock.com

STANDARDS

NCSS: Production, Distribution, and Consumption

Common Core: R.8

ECONOMICS

Should You Buy Now, Pay Later?

Many Americans are using loan apps to spread out purchase costs—often without extra fees. Is the setup too good to be true?

Question: What are some pros and cons of buy now, pay later loans?

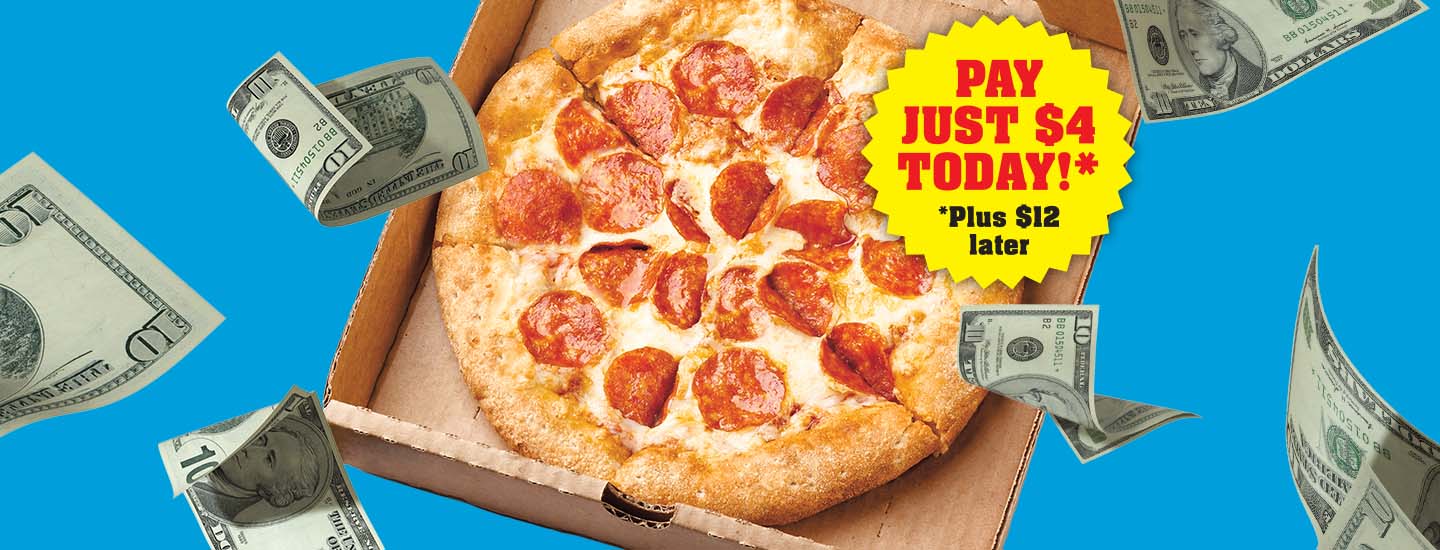

You’re starving, and your mom says you can use her DoorDash account to order pizza. When you go to check out, you’ve got two choices. One is to pay the whole $16 bill today. Another is to pay just $4 now and the rest later with something called Klarna. Wow, lunch for four bucks, you think. That’s a bargain! But is it really? And how does paying later actually work?

Klarna is one of a growing number of “buy now, pay later” (BNPL) apps. The apps let people buy goods for a fraction of their cost upfront and then pay the rest of the money over the next few weeks or months.

This type of service isn’t new, but it is becoming more common. About half of U.S. adults have used BNPL apps at least once, according to a 2025 survey from LendingTree, an online loan business.

BNPL plans may not seem like loans—no one hands you cash—but they are. The apps cover a product’s full cost when you buy it, and then you pay them back. That may sound like a great deal, especially for people who don’t have enough money right now to buy what they want.

But experts say that lower initial cost can push people into spending more than they can afford, often for things they don’t need. Products may not feel as expensive when you are only paying part of the bill at checkout, explains Bob Sullivan. He is an author who writes about consumer spending.

“A merchant offering buy now, pay later is not your friend,” Sullivan warns. “It’s using powerful psychology to encourage you to spend more than you have.”

What People Are Buying

This graph shows the top five categories in which survey respondents ages 18 to 26 made their most recent buy now, pay later purchase.

D. Hurst/Alamy Stock Photo (groceries); Shutterstock.com (all other images)

Types of Products Purchased and the Percentage of People Who Bought the Product

Clothing: 39%

Groceries: 11%

Electronics: 11%

Restaurants: 10%

Furniture: 7%

SOURCE: PYMNTS, 2023

How the Loans Work

Part of the apps’ appeal is that they are easy to use. Offers for BNPL loans pop up during checkout online and in some stores. You do have to be 18 to set up an account, which gets linked to your bank account or credit card. But the approval process takes only a minute or two, and then you can make your first purchase.

Many of the apps offer plans called “pay in 4.” These split the cost of a purchase into four equal payments over six weeks. So for that $16 pizza, you pay $4 right away. Then every two weeks, the app automatically takes $4 from your bank account or credit card. With the fourth $4 payment, the loan is repaid.

But what if you don’t have enough money to pay it off? In that case, you may be charged a late fee. Late fees are usually $7 on Zip, one BNPL app. Another app, Sezzle, charges up to $16.95 per missed payment. Some apps also tack on service fees on top of an item’s cost. If you have to pay late fees and service fees, that will end up being one pricey pizza!

And that’s just one loan. In the LendingTree poll, 23 percent of BNPL users reported having three or more of the loans at once. So while paying $4 every two weeks for the pizza might be doable, it might be harder if you’re also making $17 payments on the new Madden NFL video game and $15 payments on those jeans you just had to have.

Here to Stay

Financial experts predict that BNPL apps aren’t going away anytime soon. That’s why it’s important for even kids and teens to understand how they work, advises Nilton Porto. He’s an associate professor of consumer finance at the University of Rhode Island. “Remember that buy now, pay later is not free money,” he advises. “Every dollar borrowed must be repaid, often within just a few weeks.”

Rather than taking out BNPL loans, Porto and other experts say it’s better to focus on saving money and being thoughtful about what you do buy.

“Imagine a conversation between you today and you two months from now, when that payment is due,” Sullivan suggests. “Can you justify that purchase to Two-Months-Older-You?”

YOUR TURN

Spread the Word

What should people know about buy now, pay later apps? Using information from the article, create a poster, pamphlet, or slideshow that explains how the loans work and provides three to five tips for consumers.